The ECB’s report on harmonized wage rates, drawn from corporate data, stands out. In the second quarter, the average wage growth rate fell from 4.74% to 3.55%, which on one hand reduces the threat of a resurgence in inflation, but on the other hand, could prompt the ECB to further ease its policy.

Regarding inflation, the July report matched forecasts exactly. Core inflation, measured by the ECB’s LIMI indicator, decreased slightly from 4.4% to 4.3%. Core inflation is the primary indicator for the ECB, as it remains high amid strong activity in the services sector and is therefore expected to remain elevated for some time. High core inflation will likely restrain the ECB from lowering rates, and the market anticipates that the ECB’s rate trajectory will lag behind that of the Fed. Even if overall inflation falls to the 2% target, core inflation is expected to remain high, as is the view within both the ECB and the market, meaning there is no rush in the ECB’s actions.

Currently, the market expects a 100 basis point cut by the Fed and a 50 basis point cut by the ECB by the end of the year—in September and December, respectively. The yield gap between the dollar and the euro is expected to change by approximately 50 basis points in favor of the euro. This is currently the main factor driving EUR/USD upward, assuming no unexpected macroeconomic events occur.

The net long position on the euro increased by $4.086 billion, reaching $7.79 billion during the reporting week, indicating bullish positioning. The calculated price is above the long-term average and is confidently rising.

The economic situation in the Eurozone remains stable, with incoming data not distorting the overall assessment of the key macroeconomic indicators that could potentially alter forecasts for the euro.

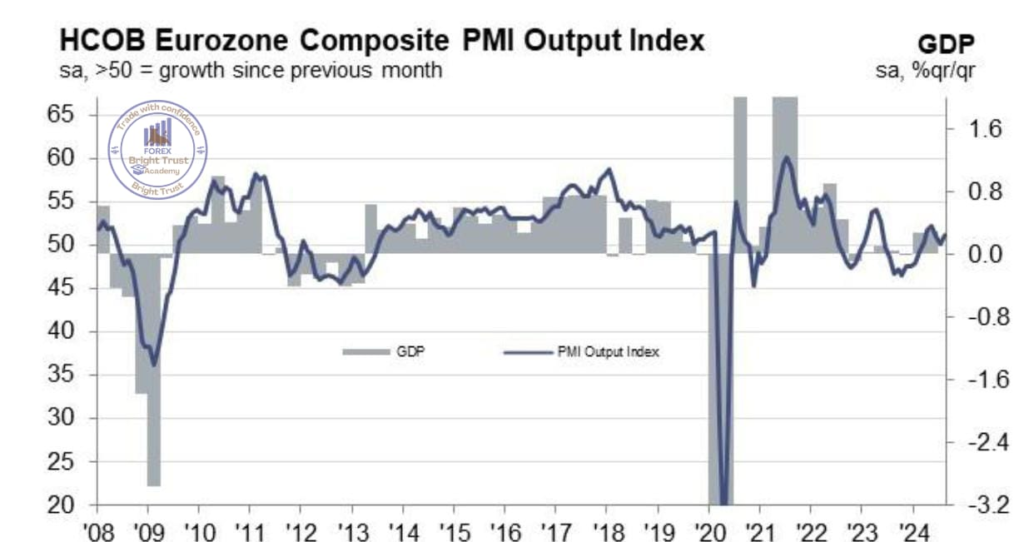

The PMI data for July generally aligned with expectations. The PMI for manufacturing fell slightly from 45.8 to 45.6 (expected 45.8), while the PMI for services rose from 51.9 to 53.3, with the growth attributed to a strong performance in France, which previously recorded weak economic performance. The increasing weakness in manufacturing could reflect a slowdown in activity in China and a subsequent decline in trade. However, there are no significant reasons to revise long-term models. The composite index increased from 50.2 to 51.2, indicating resilience in the economy, which gives the ECB room to conduct monetary policy without concern for the overall economic situation.

Bright Trust Academy